As European economies and the US are gradually reopening, the economic recovery has started. Our forecasts are comparably constructive, especially in Switzerland due to its favourable sector composition. Inflation data come in at the low end of expectations, triggering downward revisions.

Chart of the month

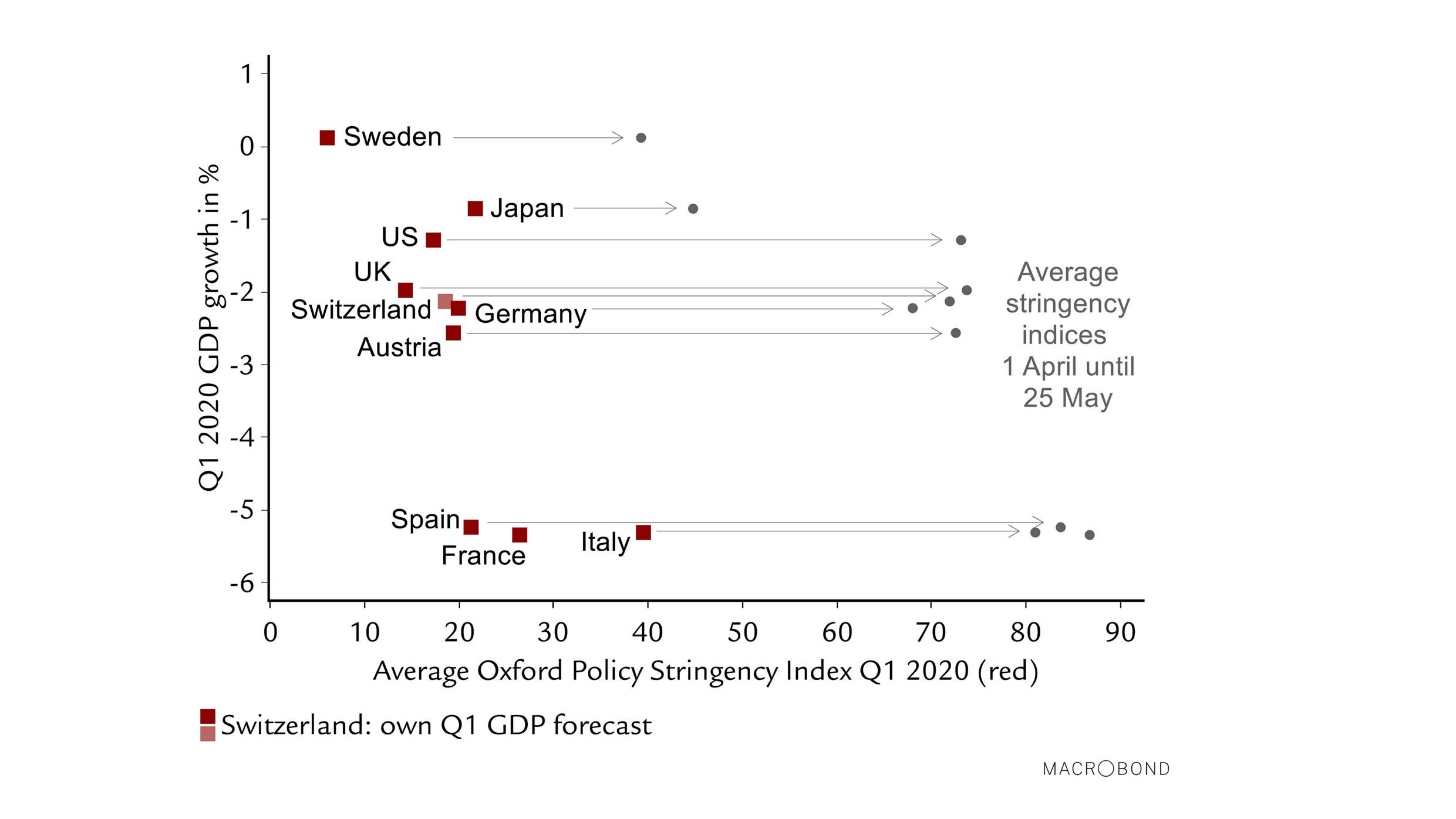

First estimates of GDP growth in the first quarter of 2020 confirmed the negative COVID-19 impact but generally surprised to the upside. Economies with stricter containment policies, as measured by the Oxford COVID-19 Stringency Index, have experienced sharper GDP contractions on average. Even though the reopening of economies is ongoing, average containment measures in Q2 will be stricter than in Q1 and most economies will therefore experience a much larger GDP drop. Nevertheless, economic data confirms the onset of a slow recovery in the second half of Q2 and we expect the hurdles for renewed nationwide, strict lockdowns to be much higher going forward.